Download the app by scanning the QR code or clicking the links below:

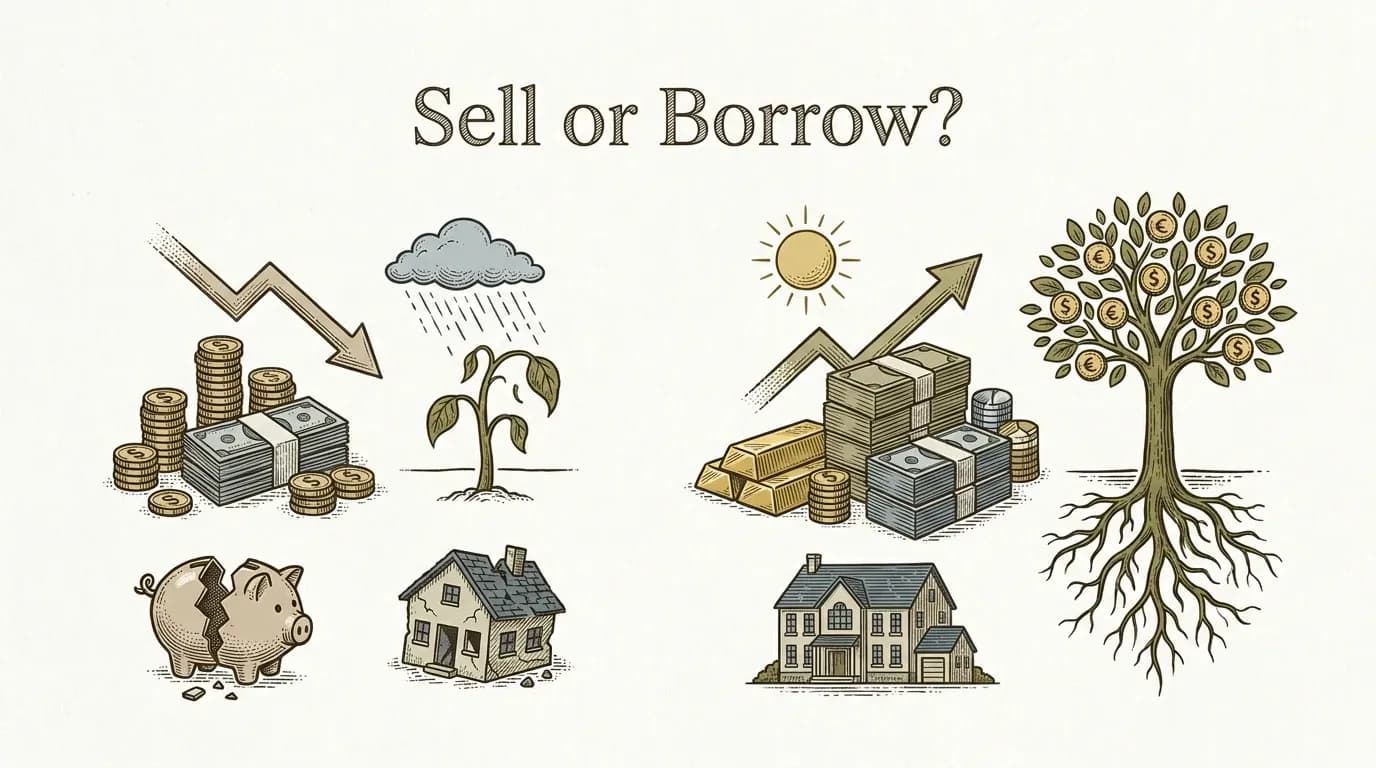

If you need cash quickly, selling your mutual funds can feel like the simplest option. The money is already yours, the redemption process is familiar, and it may seem cleaner than taking a loan.

But simple is not always cheap.

If your cash need is temporary, selling mutual funds can interrupt compounding, trigger taxes, and push you out of positions you may have spent years building. In many cases, borrowing against your mutual funds gives you the liquidity you need without forcing you to exit your investments.

This is the real decision: do you want to solve a short-term cash problem by liquidating a long-term asset, or by using that asset as collateral and staying invested?

Key Takeaways

- If your need is temporary, selling mutual funds is often the more expensive move.

- A loan against mutual funds can let you access cash while your investments keep earning returns.

- The right choice depends on how urgent the need is, how soon you can repay, and whether staying invested matters to you.

If the expense will pass and you expect to recover financially in the near term, borrowing against your mutual funds is often the stronger option.

That is because selling solves today’s cash need by giving up tomorrow’s growth. Borrowing, on the other hand, can help you cover the shortfall while keeping your portfolio in place.

If you want the full mechanics, Yenmo’s complete guide to loans against mutual funds is the best next read.

Selling mutual funds gives you immediate liquidity, but it can create costs that are easy to underestimate in the moment.

First, you reduce the amount that stays invested. If the markets recover or your fund continues compounding well, you no longer benefit on the units you sold.

Second, redemption can come with tax consequences, depending on the type of fund and your holding period. You may also face exit loads in some cases. That means the amount you lose is not always visible in one line item. Part of the cost sits in lost future returns.

Third, rebuilding the position later is not always easy. Once the immediate pressure is gone, many investors do not fully buy back what they sold. A short-term cash crunch can quietly become a long-term investing setback.

If you want to compare the two paths more concretely, Yenmo’s loan vs redemption calculator helps show the trade-off.

A loan against mutual funds works differently. Instead of redeeming your investments, you pledge them and borrow against their value.

That means your mutual funds remain invested while you access cash. For many investors, this is the core advantage. You solve the liquidity problem without fully stepping out of the market.

With Yenmo’s model, the structure is designed to feel closer to a credit line than a traditional fixed-loan experience. You can check eligibility across multiple lending partners through one platform, complete the setup digitally, and pay interest only on the amount you actually withdraw. The core offer is positioned as interest-only rather than a mandatory EMI burden.

For a product-level walkthrough, see Yenmo’s loan against mutual funds page.

Many people assume that selling your own investments must be cheaper than taking a loan. That sounds reasonable, but it is not always true.

If you sell, the visible cost may look low because no lender is charging interest. But the real cost can include taxes, exit loads, and lost future compounding. If you planned to stay invested for years, that lost growth matters.

If you borrow against your mutual funds, you do pay interest. But if the borrowing period is short and the amount is managed carefully, that cost can still be lower than the long-term cost of redeeming investments too early.

This is especially true when the loan works on a withdrawal-based structure and interest is charged only on the amount actually used.

You can also test this logic with Yenmo’s loan vs redemption calculator.

Selling is not always the wrong move.

If you no longer believe in the investment, if the money was set aside for a near-term goal anyway, or if your cash need is not temporary and repayment would be difficult, redemption may be the better choice.

You may also prefer selling if the amount is small, the tax impact is minimal, and you do not want any borrowing relationship at all.

The key is to match the tool to the situation. Borrowing works best when the need is temporary and the investment is something you genuinely want to keep.

If you want a balanced comparison, Yenmo’s loan vs redemption calculator is a practical next step.

A practical way to decide is to ask four questions.

If the need is temporary, borrowing usually deserves serious consideration. If the need reflects a lasting financial gap, selling may be cleaner than taking on debt you will struggle to repay.

If you have conviction in your long-term mutual fund plan, selling should feel expensive. Borrowing helps preserve that plan.

Do not look only at how easy redemption feels. Consider taxes, possible exit loads, and the future growth you give up.

Even a good loan is still a loan. You should be confident that the repayment structure fits your cash flow.

If you want a side-by-side comparison tool, start with Yenmo’s loan vs redemption calculator.

Often, yes, especially if you already have a meaningful mutual fund portfolio.

A personal loan is unsecured, which usually means the lender is taking more risk. For you, that can show up as a higher overall borrowing cost and a more rigid EMI structure. A loan against mutual funds is backed by your investments, so the structure can be more flexible for short-term needs.

Yenmo’s positioning is especially strong here because it emphasizes interest-only borrowing, no hidden charges, and no foreclosure or prepayment penalties as core product differentiators.

For a deeper comparison, read Yenmo’s loan against mutual fund vs personal loan guide.

No, that is one of the biggest misconceptions.

When you pledge eligible mutual funds for a loan against them, the investments remain invested. That means they can continue earning returns while pledged.

This is exactly why the product appeals to long-term investors. You do not have to choose between liquidity and staying invested in such a binary way.

If you want more background, Yenmo’s guide to loans against mutual funds expands on how pledging works.

When you are comparing borrowing with redemption, cost is only one part of the decision. Trust matters too.

You are dealing with your investment portfolio, not just a quick credit product. That is why the process, the partner ecosystem, and the fee structure matter so much.

Yenmo’s trust case includes integrations and ecosystem credibility through CAMS, KFin, NSDL, and DigiLocker, along with lending partners such as Bajaj Finance, Tata Capital, and DSP Finance. It also frames transparency as a core feature, not a footnote.

If trust is your main concern, Yenmo’s Safety and Security page is the right follow-up read.

If your need is temporary and you want to protect your long-term investing journey, borrowing against your mutual funds is often the better option.

Selling can be the right call in some situations. But for many investors, it is the easy move that turns out to be the expensive one.

If you worked hard to build your portfolio, it is worth asking one extra question before you redeem: can you solve this cash need without walking away from future compounding?

For many people, that is exactly where a loan against mutual funds fits.

If the need is temporary, selling may not be the best first option. It can interrupt compounding, create tax consequences, and reduce the long-term value of your portfolio. Borrowing against mutual funds may let you access cash while staying invested.

It can be, especially when the borrowing need is short-term. Redemption may look simple, but the real cost can include taxes, exit loads, and lost future returns. Borrowing has an explicit cost, but it may still be the lower-cost decision overall.

Yes, pledged mutual funds can remain invested and continue earning returns. That is one of the main reasons investors consider this option instead of redeeming.

Selling may make more sense if you no longer want to hold the investment, if the amount needed is small and the tax impact is low, or if repayment would be difficult and borrowing would create more stress.

For investors who already hold mutual funds, it often can be. The structure may be more efficient for short-term liquidity because the borrowing is backed by your investments rather than being unsecured.

If you need cash but still believe in your long-term investment plan, selling mutual funds should not be your automatic first move.

A temporary cash need does not always require a permanent investing setback. In many situations, borrowing against your mutual funds is the more thoughtful way to raise money because it helps you stay invested, keep earning returns, and avoid the full cost of early redemption.

Before you redeem, compare both paths carefully. The expensive option is not always the one with visible interest.